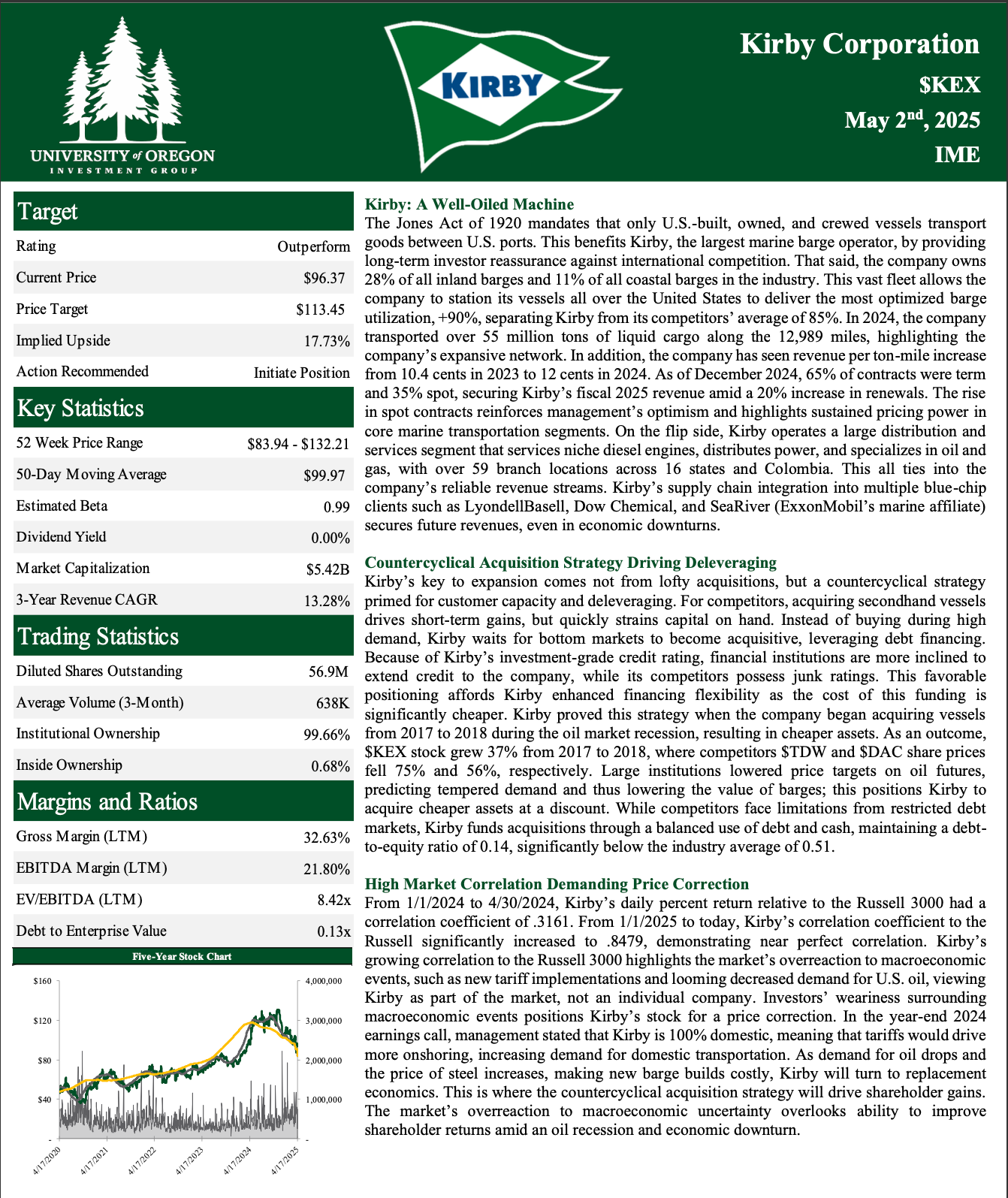

Operations

As a student run organization, the UOIG operates in a manner that is a hybrid of both an investment club and a mutual fund. The group holds weekly meetings every Friday morning of each term. During these meetings, the portfolio managers give brief presentations updating the group on the performance for the prior week. After these updates, student analysts will deliver stock presentations, recommending to either buy, hold, or sell a security. Stock reports are sent to all group members typically one week before the analyst’s presentation, giving members ample time to read and analyze the report. After each presentation, a group Q&A session follows in which everyone is given a chance to ask questions and make comments. Members will then vote on a final decision for the company, and the portfolio managers will direct the appropriate trades as decided by the majority.

Valuation

The group utilizes two primary quantitative valuation methods to estimate the intrinsic value of a company:

Comparables Analysis:

Our comparables analysis involves estimating a firm’s value by using metrics that are compared across a select number of similar companies. These metrics typically consist of dividing a company’s enterprise value by various key income line items, such as revenue, gross profit, operating income, and cash flow from operations. Comparable companies are chosen based on a variety of factors, such as similarity in risk (both macroeconomic and market-based), capital structure, revenue generation methods, and product offerings.

Discounted Cash Flows Analysis (DCF):

Our cash flow analysis is a detailed process that essentially involves projecting a company’s income statement and parts of the balance sheet, calculating quarterly and annual free cash flows, and discounting these cash flows back to the present value. We choose to measure value by the amount of free cash flow a company generates, as this represents cash that is, in essence, available to its shareholders. The UOIG primarily focuses on a long term holding period, and thus typically uses a DCF horizon of 8-10 years before reaching a terminal growth rate. The discount rate we use is our estimate of the company’s weighted average cost of capital (WACC), taking into account both the cost of equity (using the CAPM model) and the cost of debt.